How to design public venture capital funds: Empirical evidence from South Korea

sojin-lim, 김연배 (2015) · Journal of Small Business Management 53(4):843–867 · DOI ↗

한국 VC 시장 463 펀드 × 1995-2005 데이터에 mdcev 모형 적용으로 공공 VC 펀드의 NTBF 투자 효과 의 시장 단계 의존성 분석. 성장기 (1995-2000): 정부 관리 펀드 (G-gov) 가 3 세 미만 신생 firm 의 투자 촉진 (+1.14, p<0.01). 구조조정기 (2001-2005): G-gov 가 3 세 미만 신생 firm 투자 회피 (−0.83, p<0.01). 펀드 특화 (Focus) + 성과 기반 보상 (Stan, Mana) 의 dual lever 가 NTBF 투자 활성화의 핵심.

- RQ: 한국 VC 시장 의 (i) 정부 관리 펀드 (government-managed, GP-government) vs 정부 후원 펀드 (government-sponsored, LP-government) vs 민간 펀드 의 NTBF 투자 효과 차이는? (ii) VC 시장 단계 (성장기 vs 구조조정기) 가 효과를 어떻게 조절하는가? (iii) 펀드 설계 특성 (size, specialization, compensation) 의 NTBF 투자 영향?

- 방법론: mdcev (Bhat 2005 multiple discrete-continuous extreme value) — VC 펀드의 복수 firm age × industry 조합 동시 투자 + 각 alternative 의 투자 금액 결정. Baseline utility + satiation

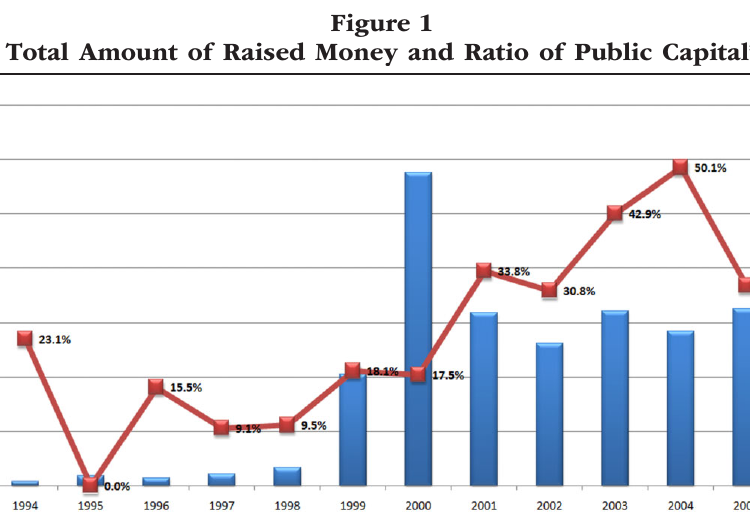

- 데이터: Korea Venture Capital Association 의 463 VC 펀드 × 1995-2005 archival 데이터. Investment alternatives: Age (A3, A3-5, A5-7, A7+) × Industry (Information, Biotech, manufacturing, Non-manufacturing). 변수: G-gov (정부 GP), Gov (정부 LP), G-cor (기업 GP), Cor (기업 LP), G-ban (은행 GP), Ban (은행 LP), Size, Focus (산업 specialization), Stan (preferred return), Mana (management fee), GP investment ratio, Down side risk, Pen (pension money), Kospi

- 주요 발견: (i) G-gov × Age 의 stage 반전: 성장기 = A3 (+1.14), A3-5 (+1.33), A7 (+1.53) 모두 양 — 공격적 early-stage 투자. 구조조정기 = A3 (−0.83), A3-5 (−1.30) 음 — risk-averse 전환. (ii) Gov × Age: 모든 단계에서 older firm 회피 + 구조조정기 younger 회피 — consistent late-stage 회피. (iii) Government × Bio industry 양의 효과 (G-gov +0.66) but × Info, Non-manuf 음의 효과 — bio 전문화. (iv) Focus 의 NTBF 효과: A3 +1.32 (whole period), Bio +0.83 — 산업 특화 = NTBF 투자 핵심. (v) Compensation 의 효과: Stan (preferred return, 음의 효과 on A3) + Mana (관리수수료, 음의 효과 on A3) — risk-sharing 부족 이 NTBF 투자 disincentive. (vi) Bank-backed (G-ban) 은 A7 (older firm) 강선호 — 예측 가능한 cash flow 선호.

- 시사점: (a) 공공 VC 의 market-stage-conditional 효과: 성장기 = 시그널 효과 + crowding-in / 구조조정기 = risk-averse 전환 + NTBF 회피. 시장 성숙도에 따른 정부 개입 design 필요. (b) 펀드 특화의 dominant lever: 산업 specialization 이 NTBF 투자 의 single most-important driver — Korea 의 generalist 정부 펀드 의 한계 evidence. (c) Compensation 의 NTBF chilling effect: 높은 preferred return + 관리 수수료 가 VC 매니저의 risk-taking 억제 — carried interest (성과 share) 기반 compensation 으로 전환 필요. (d) Bio 산업의 정부 VC 의 유일 효과적 channel: long horizon (10-15 yr) 의 private VC 의 회피 가 공공 VC 의 정당화 — bio 정부 펀드 의 정책 우선순위.

요약

본 paper 는 김연배 author page 의 제2기 (SNU-TEMEP 확장기) 의 기술 금융 분기의 핵심 작업 — Corporate Venture Capital and Its Contribution to Intermediate Goods Firms in South Korea 의 2000 boom 시기 분석 의 longer panel + finer methodology 확장 (author page 분류). 본 paper 의 conceptual move 는 — VC 펀드의 복수 firm 분산 투자 라는 multiple discrete-continuous 결정 을 mdcev (Bhat 2005) 로 modeling, 공공 vs 민간 vs 단계별 펀드 특성의 baseline utility + satiation 의 동시 식별. A forecast of household ownership and use of alternative fuel vehicles: A multiple discrete-continuous choice approach 의 자동차 다보유 가구 결정 의 VC 펀드 다투자 의사결정 으로 method transfer.

방법론 핵심은 — (i) mdcev utility: , where = baseline utility, = satiation. Budget constraint , . (ii) Kuhn-Tucker 의 0-investment vs positive-investment condition 이 discrete (which alternative) + continuous (how much) 의 simultaneous 식별. (iii) 시장 단계별 (성장기 1995-2000, 구조조정기 2001-2005) separate estimation 으로 parameter 전환 검증.

발견의 정책 함의는 공공 VC 정책 의 market-stage-conditional design. (a) 성장기의 시그널 효과: 1995-2000 의 VC bubble + 정부 공격적 투자 가 민간 펀드의 crowding-in. 정부의 promising NTBF 발굴 시그널 역할. (b) 구조조정기의 risk-aversion: 2001-2005 의 VC 시장 침체 후 정부 펀드 매니저의 risk-aversion 강화 — late-stage + 안전 firm 회피. NTBF 투자 의 gap 더 커짐. (c) Generic government fund 의 한계: Korea 의 정부 펀드가 대부분 generalist — Cumming-MacIntosh (2006) 의 crowding-out 위험 과 일치. 산업 특화 + 성과 기반 compensation 의 design 권고. (d) Bio 산업의 정부 펀드 의 일관된 양의 효과: 모든 단계에서 G-gov × Bio +0.66 (구조조정기 +0.94) — long-horizon 산업의 market failure 가 정부 개입 의 정당화. 한계: (i) 1995-2005 의 small VC market — 글로벌 비교 한계, (ii) 펀드 수익 (return) data 미사용 — NTBF 투자 의 실제 효과 (성과) 미평가, (iii) Endogeneity (펀드 type 의 historical investment 영향 무시), (iv) Penn (pension money) 같은 일부 변수의 small obs.

핵심 결과

핵심 baseline utility 계수 (MDCEV, Table 7 simplified)

| Variable | A3 (whole) | A3 (growth) | A3 (restructuring) | Bio (whole) |

|---|---|---|---|---|

| G-gov (government-managed) | −0.29 | +1.14* | −0.83* | +0.66* |

| Gov (government LP) | −0.69* | −0.67 | −1.15* | −0.87* |

| Focus (specialization) | +1.32* | +0.24 | +0.78* | +0.83* |

| Stan (preferred return) | −0.027* | +0.012 | −0.055* | +0.010 |

| Mana (management fee) | −0.51* | −0.13 | −0.93* | −0.20* |

| G-ban (bank GP) | +0.10 | +0.18 | −0.46* | −0.05 |

정량 결론. (i) G-gov 의 stage 반전: 성장기 (1.14) → 구조조정기 (−0.83) — 3 세 미만 신생 firm 투자의 시장 단계 의존성. (ii) Focus 의 universal 양의 효과: 산업 특화 가 NTBF 투자 의 dominant driver — Korea 정부 펀드의 generalist 약점. (iii) Preferred return + management fee 의 negative: risk-averse compensation 이 NTBF 투자 chilling.

방법론 노트

mdcev 의 이론적 기초는 (i) Kuhn-Tucker 의 unconstrained vs constrained alternative 의 first-order condition 이 discrete + continuous 결정의 closed form, (ii) Bhat (2005) 의 generalized translated utility 가 0 consumption 의 corner solution 식별, (iii) i.i.d. extreme value 의 random component 가 MNL-like closed-form probability.

핵심 식. VC 펀드 의 다중 투자 결정:

여기서 baseline utility, satiation. 시장 단계 별 separate estimation:

식별은 (i) MDCEV likelihood 의 closed-form (Bhat 2005 의 normalization + transformation), (ii) Industry × Age alternative cell 의 충분한 cross-section variation, (iii) Stage break (2000-2001) 의 VC bubble burst exogenous shock.

연구 계보

본 paper 는 (a) Lerner (1999, 2002), Gompers-Lerner (1999, 2001), Cumming-MacIntosh (2006), Cumming (2007), Grilli-Murtinu (2011), Bertoni-Tykvová (2012) 의 공공 VC 정책 효과 literature, (b) Hellmann-Puri (2002), Manigart et al. (2002), Chesbrough (2002) 의 VC source heterogeneity literature, (c) Bhat (2005), A forecast of household ownership and use of alternative fuel vehicles: A multiple discrete-continuous choice approach 의 MDCEV 방법론 literature 의 결합. Corporate Venture Capital and Its Contribution to Intermediate Goods Firms in South Korea 의 Korean VC 시장 (1999-2001 boom) 분석을 longer panel (1995-2005) + MDCEV 의 simultaneous design feature 모형화 으로 확장한 직접 후속작. 김연배 author page 의 제2기 기술 금융 라인의 핵심 작업 (author page 분류). 기술경영경제정책전공 의 MDCEV 방법론 라인 — A forecast of household ownership and use of alternative fuel vehicles: A multiple discrete-continuous choice approach (AFV) → 본 paper (VC) 의 application 다양화.

See also

- mdcev

- public-venture-capital

- new-technology-based-firms

- equity-gap

- 한국 벤처캐피탈 시장

- vc-fund-design

- sojin-lim

- 김연배

- Corporate Venture Capital and Its Contribution to Intermediate Goods Firms in South Korea

- A forecast of household ownership and use of alternative fuel vehicles: A multiple discrete-continuous choice approach

- Journal of Small Business Management

인접 그래프

- 인물 1

- 개관 1

- 방법론 1

- 주제 1

- 수록처 1

- 분류 2

- 논문 2