Crude oil inventories: The two faces of Janus?

Soohyeon Kim, Jungho Baek, 허은녕 (2020) · Empirical Economics · DOI ↗

원유 재고가 (i) 시장 buffer 인지 (ii) speculative trading 의 facilitator 인지를 구조 벡터자기회귀(SVAR) 에 부호 제약 을 가해 동일 framework 에서 동시 식별한다. Global·US·Cushing 의 세 aggregation level 에서 2003.1–2008.6 과 2009.1–2018.5 두 시기를 비교하고, supply/demand shock 에 대한 재고의 즉각·점진 buffer 반응 과 Cushing 특유의 즉각 speculative 반응을 IRF 로 보인다.

- RQ: 원유 재고는 oil supply/demand shock 에 buffer 로 반응하는가, speculation facilitator 로 반응하는가, 또는 둘 다인가? aggregation level (Global / US / Cushing) 과 시기 (2003–2008 vs 2009–2018) 별로 어떻게 달라지는가?

- 방법론: 구조 벡터자기회귀(SVAR), 부호 제약, 시변계수 VAR (확률 변동성) (robustness)

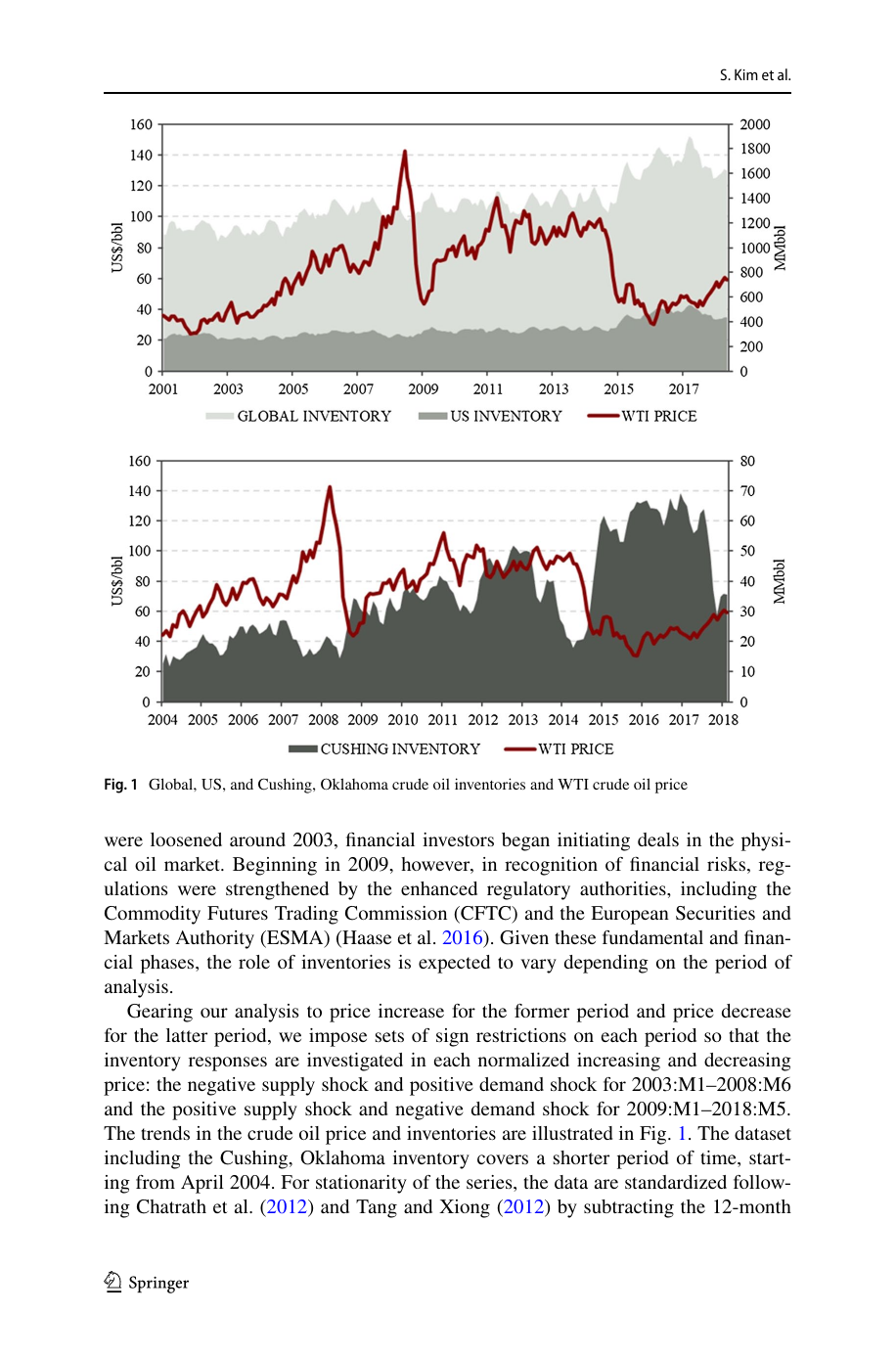

- 데이터: WTI 실질 가격, 세계 원유 생산·소비, Global·US·Cushing 원유 재고 (EIA), 월별 표준화 자료. Period 1: 2003.1–2008.6 (N=66); Period 2: 2009.1–2018.5 (N=113). Cushing 만 2004.4 이후.

- 주요 발견: 2003–2008 — Global·US 재고는 negative supply shock 에 즉각 speculative (+0.12, +0.13) 후 점진 buffer 반응, positive demand shock 에는 즉각 buffer (-0.14, -0.20) 후 speculative. Cushing 은 양 shock 모두 즉각 speculative (+0.21, +0.13). 2009–2018 — 모든 재고가 oversupply 흡수의 buffer 역할 dominant. FEVD 에서 demand vs supply shock 기여도는 Cushing 의 2003–2008 demand shock 11.9% (supply 6.6%) 가 두드러짐.

- 시사점: 재고의 buffer/speculative 역할은 aggregation level 과 시기에 의존. Cushing hub 의 speculative 채널이 dominant 인 사실은 정책 규제 (US Senate 2014, FRB, CFTC) 의 근거를 academic 으로 뒷받침.

Fig. 1. Global·US·Cushing 원유 재고와 WTI 실질가격 추이 — 두 분석 시기 (2003–2008 가격 급등, 2009–2018 셰일 글러트) 의 구조적 차이를 시각화.

요약

원유 재고 연구는 buffer-stock 시각 (Kaldor 1939, Fama-French 1988, Pindyck 2001, Williams-Wright 1991, Considine 1997) 과 speculation 시각 (Hamilton 2009, Kilian-Murphy 2014, Kilian-Lee 2014, Singleton 2014, Juvenal-Petrella 2015, Ederington et al. 2018) 두 갈래로 갈렸으나, 두 효과를 동일 분석에서 endogenous response 로 식별한 연구는 드물었다. 본 paper 는 Soohyeon Kim · 허은녕 라인이 자원 시장의 재고-가격 dynamics 를 구조 벡터자기회귀(SVAR) 로 분석하면서, 재고의 speculation 충격 자체를 exogenous 로 가정한 Kilian-Murphy 류와 달리 supply/demand shock 에 대한 재고의 endogenous response 가 buffer/speculative 부호를 결정하도록 식별 전략을 재구성.

부호 제약 identification (Uhlig 2005, Rubio-Ramirez et al. 2010) 은 reduced-form VAR 의 shock 을 economic theory 의 부호 (supply shock 은 production↑, price↓; demand shock 은 consumption↑, price↑) restriction 으로 분리. Bayesian QR decomposition 으로 1,000 draws 의 admissible rotation 을 추출. 4-변수 SVAR (production, consumption, inventory, price) 을 Global·US·Cushing 각 수준에서 추정. 표준화 (12개월 평균 차감 후 표준편차 분할) 로 scale 차이 흡수. Cholesky 의 a priori ordering 가정을 회피.

결과는 시기·level 별로 분명한 차이. 2003–2008 (가격 급등기): Global·US 재고가 negative supply shock 에 첫 1–3 개월 positive (speculative hoarding) 후 4 개월부터 negative (buffer release); positive demand shock 에는 첫 3 개월 negative (buffer) 후 4 개월부터 positive (speculative continuation). Cushing 은 양 shock 모두 즉각 양의 응답 — 즉시 speculative. 2009–2018 (셰일 글러트): Global·US 재고가 positive supply shock 에 positive 응답하며 oversupply 를 흡수하는 buffer 역할이 dominant. Cushing 만 2014 부근에서 sell-off 형태의 speculative 거동 (TVP-VAR-SV 와 ADS index alternative 분석에서 더 분명하게 surfaces).

이 paper 는 Soohyeon Kim 의 자원 가격 dynamics 라인 (Kim, Kim, Heo 2014, 2017 의 convenience yield 분석) 의 직접 후속이며, Speculative incentives to hoard aluminum: Relationship between capital gains and inventories 가 같은 buffer vs. speculation 질문을 알루미늄 시장에 동적 선형 모형 / 시변계수 VAR (확률 변동성) 로 확장한다. 정책 함의는 commodity speculation regulation 의 academic 근거 — 재고의 primary 역할 (buffer) 이 speculation 에 의해 overwhelmed 될 때 producers·consumers 가 손해를 본다는 energy justice 관점.

핵심 결과

FEVD (forecast error variance decomposition, 12개월 평균, %) 에서 supply 와 demand shock 이 재고 변화에 기여하는 비율 (Table 2):

| 시기 | Shock | GLOBAL | US | CUSHING |

|---|---|---|---|---|

| 2003–2008 | Supply | 8.6 | 7.0 | 6.6 |

| 2003–2008 | Demand | 7.8 | 7.5 | 11.9 |

| 2009–2018 | Supply | 16.9 | 15.4 | 7.9 |

| 2009–2018 | Demand | 14.1 | 16.7 | 6.2 |

핵심 IRF peak (median, 1 standard deviation shock 후):

- 2003–2008 negative supply shock → Global +0.12, US +0.13 (3개월차 peak, speculative); Cushing 은 1개월차 +0.21 즉각 speculative.

- 2003–2008 positive demand shock → Global -0.14, US -0.20 (buffer, 1–3개월); Cushing 은 +0.13 hump-shaped (speculative).

- 2009–2018 positive supply shock → US +0.21 즉각 (US 가 셰일 epicenter); Global·CUSHING 도 buffer-positive 영역으로 진입.

방법론 노트

부호 제약 SVAR 의 핵심은 reduced-form VAR 의 white-noise error 가 economic 의미를 갖는 structural shock 와 행렬 로 연결된다는 가정:

식별 절차: Cholesky-decompose → orthonormal impulse vector 를 QR decomposition 으로 생성 → 곱해 얻은 IRF 가 사전 정의된 sign restriction (예: negative supply shock 은 production↓ + price↑) 을 만족하면 keep, 아니면 discard. Bayesian framework 에서 normal inverted-Wishart posterior 로 부터 VAR parameter draw, 1,000 회 반복.

식별된 shock 의 부호 약속:

- Negative supply shock: production ↓, consumption ↓, price ↑.

- Positive supply shock: production ↑, consumption ↑, price ↓.

- Positive demand shock: consumption ↑, production ↑, price ↑.

- Negative demand shock: consumption ↓, production ↓, price ↓.

재고의 response 가 speculative 인지 buffer 인지는 부호로 판정 — 수요 > 공급 상황에서 재고가 +면 speculative (arbitrage hoarding), -면 buffer (release). 공급 > 수요 상황에서 +면 buffer (absorb glut), -면 speculative (sell-off).

Robustness: (i) demand variable 을 IP index, ADS business condition index 로 교체; (ii) sign restriction duration 을 12 → 6 개월; (iii) TVP-VAR-SV (Primiceri 2005, Baumeister-Peersman 2013) 로 time-varying coefficient 와 stochastic volatility 동시 허용. 세 robustness 모두 baseline 의 정성 결론을 지지하며, 특히 TVP-VAR-SV 가 2014 sell-off 같은 단기 speculative episode 를 추가로 surface.

연구 계보

Kilian-Murphy (2014), Kilian-Lee (2014) 의 speculation-focused VAR 라인 — 글로벌 oil price 의 2003–2008 surge 를 speculative inventory shock 으로 설명 — 과 Hubbard-Weiner (1986), Williams-Wright (1991), Deaton-Laroque (1992), Considine (1997) 의 buffer-stock optimization 라인을 동일 SVAR framework 안에서 통합. Juvenal-Petrella (2015), Beidas-Strom-Pescatori (2014), Güntner (2014), Lombardi-Van Robays (2011) 의 후속 speculation SVAR 들이 모두 inventory speculation 을 exogenous 로 가정한 데 반해, 본 paper 는 inventory 의 endogenous 반응으로 동일 결론을 도출. 동일 저자의 soohyeon-kim-2014-convenience-yield-energy-market (Kim, Kim, Heo 2014) 와 soohyeon-kim-2017-china-copper-convenience-yield (Kim, Kim, Heo 2017) 의 convenience yield 라인이 직접 선행. 허은녕 의 3기 (2018~2024) 자원 시장 미시구조 분석 라인의 핵심 paper.

See also

- Speculative incentives to hoard aluminum: Relationship between capital gains and inventories

- 구조 벡터자기회귀(SVAR)

- 부호 제약

- 시변계수 VAR (확률 변동성)

- 원유 재고

- 투기적 재고

- 재고 이론

- Soohyeon Kim

- 허은녕

- Empirical Economics

인접 그래프

- 인물 3

- 방법론 4

- 개념 1

- 주제 2

- 수록처 2

- 논문 2