Effects of environmental regulations on trade flow in manufacturing sectors: Comparison of static and dynamic effects of environmental regulations

jungah-hwang, 김연배 (2017) · business-strategy-and-the-environment 26(5):568–577 · DOI ↗

환경 규제의 static vs dynamic 효과를 export + import + environmental innovation 의 3-equation framework 로 검증. 19 OECD 국 × 1996-2009 panel + 중력 모형 (manufacturing trade) + environmental innovation equation. Energy tax 의 static effect: 모든 industry group 에서 exports 감소 (HG −0.15, MG −0.07). Dynamic effect: energy tax → environmental knowledge stock ↑ → exports ↑ (positive). 그러나 positive dynamic 이 negative static 을 offset 못 함 — partial Porter hypothesis 만 지지. ETS 는 모든 group 에서 exports + — 그러나 free + excess allowance 의 artifact 가능.

- RQ: 환경 규제 (environmental tax, energy tax, ETS, CO₂ intensity) 가 (i) static 으로 export/import 에 어떻게 영향? (ii) dynamic (environmental innovation 매개) 으로 어떤 spillover? (iii) Porter hypothesis (innovation offset) 가 정량적으로 성립하는가?

- 방법론: 2-model framework. Model 1: 중력 모형 의 trade flow = f(GDP, distance, tariff, RTA, environmental regulation). Model 2: Environmental innovation = f(prior knowledge, environmental tax, energy tax, ETS, public R&D). 영구재고법 의 environmental knowledge stock. 패널 고정효과 모형

- 데이터: 19 OECD 국 × 1996-2009 panel. 3 산업 그룹 — HG (high-energy), MG (medium-energy), LG (low-energy). Environmental regulation: tax (환경세, 에너지세), ETS dummy. Innovation: energy-related patents

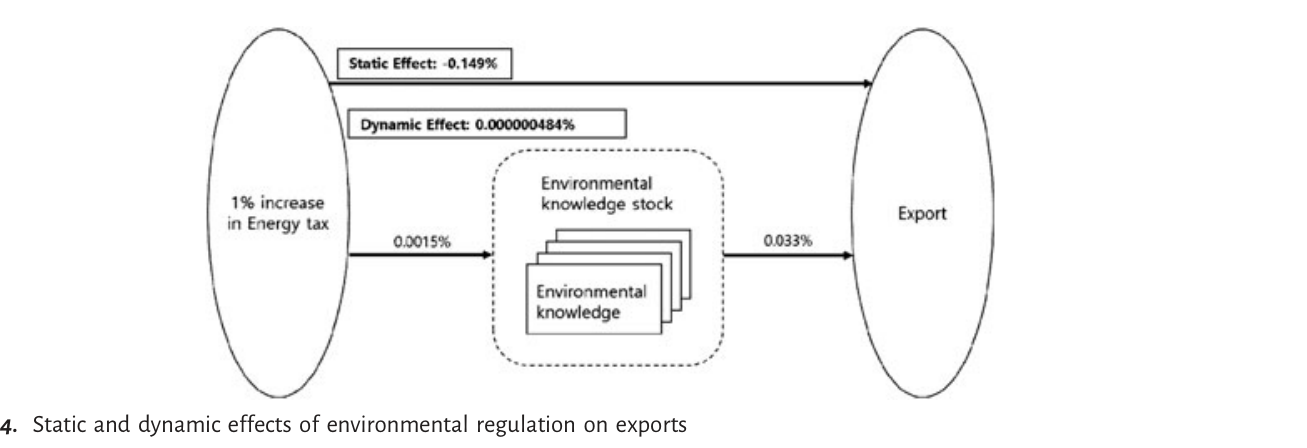

- 주요 발견: (i) Static export effect: 환경세·에너지세 대부분 group 에서 음의 유의. HG: environmental tax −0.13, energy tax −0.15 (각 p<0.01). LG: env tax −0.15, ETS는 모든 group 에서 양의 유의 (HG +0.16, MG +0.17, LG +0.03). (ii) CO₂ intensity effect: 모든 group 에서 exports 음의 유의 (Porter-supporting — 친환경 firm 이 더 경쟁력). (iii) Imports: 환경 규제가 imports 감소 효과 — non-tariff barrier 역할. (iv) Dynamic effect (Model 2): energy tax → environmental knowledge +0.007* (p<0.10) — induced innovation 입증. 그러나 environmental tax, ETS 는 knowledge creation 에 비유의. (v) Static vs Dynamic offset: HG 의 energy tax 1% 증가 → exports −0.149%, environmental knowledge +0.0015% → induced innovation 의 export 회복은 미미. Porter hypothesis partial 지지 — full offset 안 됨.

- 시사점: (a) Energy tax 의 induced innovation 정량 evidence: 에너지세가 technology-push 정책처럼 작동, 그러나 export recovery 의 magnitude 충분치 않음. (b) ETS 의 export-promoting artifact 의 caveats: 현 EU ETS 의 free + over-allocation 으로 가격 너무 낮음 — actual cost 부담 없는 effective subsidy 가능성. (c) Non-tariff barrier 효과 의 정량 식별: WTO Article XX 의 환경 예외 가 de facto trade barrier 로 작동. (d) Porter hypothesis 의 partial 지지: CO₂ intensity → exports 의 long-run virtuous cycle 확인, 그러나 tax-induced innovation 의 short-run 으로 full offset 불가. Porter 의 firm-level 명제 vs industry-aggregate 효과의 gap.

요약

본 paper 는 김연배 author page 의 제2기 (SNU-TEMEP 확장기) 의 환경 정책 + 무역 라인 의 mid-stage milestone (author page 분류). Why do consumers respond to eco-labels? The case of Korea (SpringerPlus, 일반 소비자 eco-label) 의 consumer-side environmental behavior 분석을 industry-side trade + innovation 으로 scale-up. Role of policy in innovation and international trade of renewable energy technology: Empirical study of solar PV and wind power technology 의 재생에너지 R&D-trade 분석 의 환경 규제 일반화. 본 paper 의 conceptual move 는 — Porter-van der Linde (1995) 의 innovation offset 명제의 정량 검증 (induced innovation 정량 측정 + dynamic export effect 계산 → offset 정도 비교).

방법론은 2-equation 분리 추정. (i) Model 1 (Gravity-trade): — 중력 모형 에 환경 변수 추가. (ii) Model 2 (Innovation): — 영구재고법 의 environmental knowledge stock. (iii) Comparison: Static (Model 1 의 tax coefficient) + Dynamic (Model 1 의 K_env coefficient × Model 2 의 tax coefficient) 의 합산 비교 — Porter offset 정도 계산.

발견의 정책 함의는 *환경 규제 정책의 full Porter offset 의 미신. (a) Single-instrument 한계: 에너지세 의 negative export effect 가 induced innovation 의 positive offset 보다 크다 — *single tax 만으로는 international competitiveness 유지 불가. Tax + R&D subsidy + 보호 무역 의 policy mix 필요. (b) ETS 의 misleading positive: 현 ETS 의 free allocation + low price 로 실질 cost 부담 없음 — *positive export effect 가 real regulatory effect 아님. ETS reform (auction, price floor) 필요. (c) Heterogeneity by industry group: HG (high-energy) 가 부담 큼 + innovation 동기 큼 — Porter hypothesis 의 HG-specific 부분 지지. LG 는 export effect 작음 + innovation 영향 작음. (d) CO₂ intensity 의 firm-level competitive advantage: 친환경 firm 의 brand premium + cost reduction 의 export benefit — firm-level Porter 만 robust 지지. 한계: (i) 19 OECD 국 only — developing country pollution haven 미포함, (ii) Patent 만 innovation metric, (iii) ETS allowance price 의 time variation 미반영 (binary dummy), (iv) Endogeneity (high-tax 국가 의 self-selection of cleaner manufacturing).

핵심 결과

Model 1 — Gravity-trade 추정 (Table 6, HG/MG/LG 비교)

| 변수 | HG (1) | MG (3) | LG (5) |

|---|---|---|---|

| Environmental tax (exporter) | −0.128* | +0.001 (n.s.) | −0.149* |

| Energy tax (exporter) | −0.149* | −0.071* | −0.026 (n.s.) |

| ETS dummy | +0.162* | +0.170* | +0.027* |

| ln K_env (env knowledge) | +0.033* | −0.011 | +0.021* |

Model 2 — Environmental innovation (Table 7)

| 변수 | 계수 | 유의 |

|---|---|---|

| Prior knowledge stock(t−1) | +0.0001* | p<0.01 |

| Environmental tax | +0.057 | n.s. |

| Energy tax | +0.0069* | p<0.10 |

| ETS | +0.011 | n.s. |

| Public R&D | +0.001* | p<0.01 |

Static vs Dynamic Offset (HG, energy tax 1% 증가 시)

| 효과 | 값 (% change in exports) |

|---|---|

| Static (direct tax → exports) | −0.149% |

| Dynamic (tax → K_env → exports) | +0.0015% × 0.033 = +0.00005% |

| Total | −0.149% (offset 거의 없음) |

정량 결론. (i) Energy tax 의 induced innovation 은 통계적으로 식별 (+0.0069), 그러나 export-side magnitude 가 매우 작아 full offset 불가. (ii) ETS 의 export-positive (+0.16) 가 true policy effect 가 아닌 free allocation artifact 가능. (iii) Environmental tax 는 export 에는 negative, innovation 에는 비유의 — energy 와 environmental tax 의 instrument heterogeneity.

방법론 노트

중력 모형 의 trade flow 와 innovation-equation 의 environmental innovation 의 분리 추정. Static effect = Gravity model 의 tax coefficient. Dynamic effect = Innovation equation 의 tax coefficient × Gravity model 의 K_env coefficient. Porter offset 비율 = |Dynamic / Static|.

핵심 식. Gravity-trade:

여기서 = market size, = environmental/energy tax, = environmental knowledge stock. Environmental innovation:

영구재고법: , . 식별은 (i) Gravity model 의 fixed effects (importer × exporter × year), (ii) Innovation equation 의 country-specific control (Gov, Size 같은 NSI indicator), (iii) Energy/environmental tax 의 cross-country variation + within-country variation 의 sufficient panel structure.

연구 계보

본 paper 는 (a) Porter-van der Linde (1995), Jaffe-Palmer (1997) 의 Porter hypothesis + induced innovation literature, (b) Grossman-Krueger (1991), Tobey (1990), Levinson-Taylor (2008), Ederington et al. (2005), Eskeland-Harrison (2003), Antweiler-Copeland-Taylor (2001), He (2006) 의 environmental regulation + trade literature, (c) Frondel et al. (2007), Newell-Jaffe-Stavins (1999) 의 environmental tax + innovation literature, (d) Demailly-Quirion (2006), Goh (2004), Kiuila (2015) 의 environmental regulation as non-tariff barrier literature 의 통합. Static vs Dynamic offset 의 정량 비교 가 distinctive contribution. jungah-hwang 의 두 번째 first-author paper — Why do consumers respond to eco-labels? The case of Korea (SpringerPlus, consumer-side) 의 자매 (industry-side). 김연배 author page 의 제2기 환경 정책 라인의 trade 차원 (author page). Role of policy in innovation and international trade of renewable energy technology: Empirical study of solar PV and wind power technology (RSER) 의 재생에너지 specific 분석 의 환경 정책 일반화. 기술경영경제정책전공 의 환경 규제 + 무역 + 혁신 의 3-axis 라인의 milestone.

See also

- 중력 모형

- 영구재고법

- 패널 고정효과 모형

- porter-hypothesis

- environmental-regulation

- energy-tax

- emissions-trading-system

- induced-innovation

- non-tariff-barrier

- jungah-hwang

- 김연배

- Why do consumers respond to eco-labels? The case of Korea

- Role of policy in innovation and international trade of renewable energy technology: Empirical study of solar PV and wind power technology

- business-strategy-and-the-environment

인접 그래프

- 인물 1

- 개관 1

- 방법론 3

- 주제 1

- 분류 1

- 논문 3