R&D Dynamics and Firm Growth: The Importance of R&D Persistency in the Economic Crisis

Hayoung Park, Taewon Kang, 이정동 (2019) · International Journal of Innovation Management 23(5):1950049 · DOI ↗

기술경영경제정책전공 의 축적 (accumulation) → R&D 동학 anchor 라인을 위기 환경 으로 확장한다. 2008-2009 글로벌 금융위기 위기와 회복기 (2010-2011) 의 글로벌 석유화학 산업 1,137 기업 균형 패널 에서 위기 중 R&D 투자를 ±5% 범위 안에서 유지한 firm (109 개, 9.7%) 의 성장률이 변동시킨 firm (1,027 개) 보다 위기·회복기 모두 유의하게 높았다. R&D 지속성 계수 +0.226 ~ +0.408 (모두 p<0.01), 영향은 대기업 에서 더 큼 (+0.227 vs 소기업 +0.179). R&D 변동성 의 reduction 도 increase 도 모두 firm 성장에 부정적 — 수준 이 아니라 동학 이 결정 변수. Bloom (2007) 의 caution effect 와 R&D 스무딩 (Brown and Petersen 2011) 가설을 정량 지지.

- RQ: 글로벌 금융위기 환경에서 firm 의 R&D 투자 수준 (level) 보다 동학 (dynamics), 특히 R&D 지속성 가 firm 성장에 더 결정적인가? 그 효과는 firm size 에 따라 어떻게 다른가?

- 방법론: Hausman-Taylor 추정량 (time-invariant key variable + endogeneity 처리), 균형 패널, pre-crisis high-growth dummy 비교, robustness 로 continuous R&D volatility (3-year sliding window σ) 추가 추정

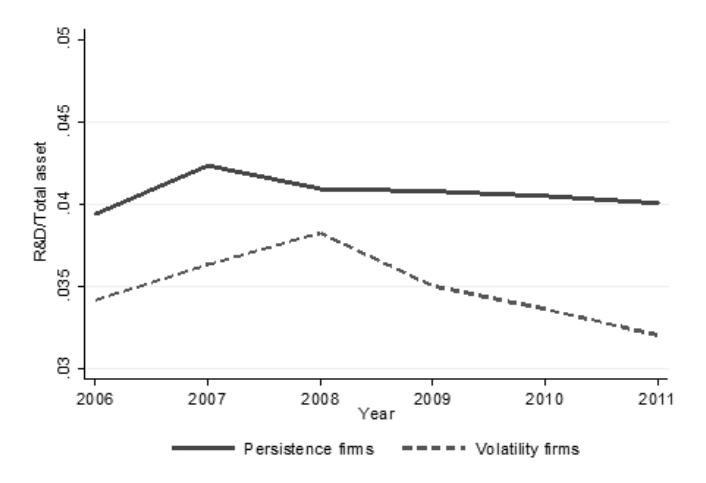

- 데이터: Bureau van Dijk ORBIS, 전세계 석유화학 산업 N=1,137 firms × 6 years (2006-2011) = 4,548 obs, 위기 기간 정의 2008-2009 (회복기 2010-2011)

- 주요 발견: 1,137 firm 중 109 (9.7%) 가 위기 중 R&D 강도와 ln(R&D) 모두 ±5% 범위에서 유지 (R&D 지속 그룹). 지속 그룹은 전 기간 (Model 1) 성장률 +0.226, 위기 (Model 2) +0.408, 회복 (Model 3) +0.286 (모두 p<0.01) 만큼 변동 그룹보다 높음. Pre-crisis high-growth (top 10%) 는 위기·회복기 모두 비유의 — 위기 환경에서 경로 의존성 단절. 대기업 (median 이상) +0.227 vs 소기업 +0.179 — 대기업이 R&D 스무딩 으로 더 큰 이득. R&D 변동성 (3-year σ) 계수 -0.018 ~ -0.031 (p<0.05) 로 변동성 자체가 성장 저해.

- 시사점: 위기 시 R&D 를 늘리는 공격적 전략도, 줄이는 방어적 전략도 모두 firm 성장에 부정적. 진정한 R&D 스무딩 (변동 최소화) 가 결정적. 정부는 위기 시기 한정 R&D 보조금 으로 firm 의 R&D 지속성 를 유지시켜야 (Paunov 2012).

요약

R&D 동학 에 대한 두 흐름 — persistency 진영 (Dierickx and Cool 1989, Bernstein and Nadiri 1989, Himmelberg and Petersen 1994 의 조정비용·매몰비용·time compression diseconomy) 과 volatility 진영 (Mudambi and Swift 2011, 2014, Cincera et al. 2016 의 proactive R&D management + 내부 현금흐름 민감도) — 의 위기 환경 검증 이 학계의 빈자리였다. 기존 위기 연구는 변동의 방향 (감소 / 증가) 만 다루고 변동 자체의 비용 을 누락했고 (Colombo et al. 2016, Eberhart et al. 2004, Amore 2015), Bloom (2007) 의 caution effect (높은 불확실성 하 R&D 유지) 와 Brown and Petersen (2011) 의 R&D 스무딩 (cash holdings 으로 충격 완충) 가설은 위기 데이터로 직접 검증되지 않았다. 본 paper 는 기술경영경제정책전공 의 축적 (accumulation) → R&D 동학 anchor 라인 (이정동 author page anchor 의 제3기 (3) accumulation 라인) 을 2008-2009 글로벌 금융위기 환경 으로 확장한 작업으로, The persistency and volatility of the firm R & D investment: Revisited from the perspective of technological capability 의 비대칭 매출 충격 + TC 조절 framework 을 위기 vs 회복기 / 대기업 vs 소기업 의 cross-cutting 환경 분해로 확장한다.

데이터는 Bureau van Dijk ORBIS 의 글로벌 석유화학 산업 (cyclical 산업, 위기 직접 영향) 1,137 firm 의 균형 패널 (2006-2011, 4,548 obs). 핵심 explanatory variable Per_Group dummy 는 위기 (2008-2009) 평균 ln(R&D) 와 R&D/총자산 비율 모두 사전 (2006-2007) 평균의 ±5% 범위 안에서 유지된 firm 으로 정의 (Amore 2015 의 5% threshold). 추정은 Hausman-Taylor 추정량 — time-invariant 인 Per_Group 과 Highfirm 을 fixed effect model 에서 추정 불가능한 문제와, R&D 동학·firm 성장 사이의 endogeneity 를 IV 로 동시 해결하는 estimator. 결과는 모든 기간 (Model 1) 에서 Per_Group 계수 +0.226 (p<0.01), 위기기 (Model 2) +0.408, 회복기 (Model 3) +0.286 — 위기 중 의 효과가 가장 크다. Highfirm (pre-crisis top 10%) 은 모두 비유의 — 위기가 경로 의존성을 단절. Size 분할에서 large firm 계수 +0.227 > small firm +0.179 — 대기업이 복잡한 organizational structure 때문에 sudden 변동의 비용이 더 크고 R&D 스무딩 의 이득도 큼. Robustness 로 continuous R&D 변동성 (3-year sliding window σ of ln R&D 성장률, Frankish et al. 2013) 계수 -0.023 (p<0.01) — 변동성 자체가 성장에 negative.

한계는 (i) firm-level 만 분석, 프로젝트 수준 R&D 동학 미관측 — 어떤 프로젝트를 stop / continue 하는가 의 미시 portfolio 가 R&D 지속성 의 진정한 결정 layer, (ii) 석유화학 산업 단일 — 기술 변화 빠른 산업 (electronics, biotech) 에서는 proactive volatility 가 오히려 이득일 가능성 (Mudambi and Swift 2011), (iii) post-crisis window 가 2년뿐 — 더 긴 시계열로 long-term 효과 검증 필요. 기술경영경제정책전공 의 R&D 동학 anchor 라인 sibling 으로 The persistency and volatility of the firm R & D investment: Revisited from the perspective of technological capability (TC 조절자 mechanism), R&D activities for becoming a high-growth firm through large jumps: evidence from Korean manufacturing (large jump 모멘텀 단계 분해), Effects of knowledge accumulation strategies through experience and experimentation on firm growth (지식 composition 의 experience-experimentation 분해) 가 동일 anchor 라인의 환경·단계·composition 의 cross-section 분화로 위치한다.

핵심 결과

Hausman-Taylor 추정량 결과 (N=4,548, 1,137 firms × 6 years, threshold [-5%,+5%]):

| 기간 | Per_Group (R&D 지속) | Highfirm (pre-crisis top 10%) | R&D_Inten (t-1) |

|---|---|---|---|

| 전 기간 2008-2011 (M1) | +0.226*(0.028) | -0.964 (1.158) | -0.205*** (0.065) |

| 위기 2008-2009 (M2) | +0.408*(0.050) | -1.398 (2.074) | -0.117 (0.102) |

| 회복 2010-2011 (M3) | +0.286*(0.036) | -1.123 (1.460) | +0.011 (0.142) |

Size 분할 (위기·회복 통합, M1):

- Small firm (median 이하, n=569): Per_Group +0.179*** (0.047)

- Large firm (median 이상, n=568): Per_Group +0.227*** (0.088)

Robustness (continuous R&D volatility): Vol_R&D 계수 -0.023*** (전 firm), -0.018** (소), -0.031*** (대) — 모든 그룹에서 변동성이 성장 저해.

위기 사전 (2006-2007) high-growth firm (top 10%) 도, 위기 중 R&D 수준 (R&D/매출) 도 모두 비유의 — R&D 동학 만이 firm 성장의 결정 변수.

방법론 노트

Hausman-Taylor 추정량 의 핵심 motivation 은 time-invariant key variable (Per_Group, Highfirm) 의 패널 고정효과 모형 추정 불가능성 + R&D 동학과 firm 성장 간의 endogeneity (R&D 결정이 미관측 firm 특성에 의존). Hausman and Taylor (1981) 의 estimator 는 random-effects transformation 위에서 time-variant exogenous variable 의 individual mean 을 time-invariant variable 의 IV 로 사용한다.

추정식:

여기서 의 매출 성장률, Per_Group 은 위기 중 ln(R&D) 와 R&D/총자산 의 두 dimension 모두에서 사전 평균 ±5% 안에 머문 firm 의 dummy (Amore 2015 의 R&D-stable 정의 확장).

식별 핵심: Per_Group 은 사전 (2006-2007) 정보 + 위기 중 (2008-2009) 변동성 으로 결정돼 사후 (2010-2011) 성장률 외생. Highfirm 도 사전 분류 이므로 위기·회복기 결과변수와 외생. Hausman test 는 fixed-effects 가 적합하나 time-invariant variable 미추정 가능, Hausman-Taylor 가 IV approach 로 해결. Threshold 민감도는 [-3%,+3%] / [-7%,+7%] 에서도 모두 유의 + 결과 일관. Continuous robustness (Vol_R&D = 3-year σ) 도 동일 결론.

연구 계보

본 paper 는 기술경영경제정책전공 의 축적 (accumulation) → R&D 동학 anchor 라인 (이정동 author page anchor 의 제3기 (3) accumulation 의 학술적 기반 구축) 의 위기 환경 확장 이다. 직접 선조는 The persistency and volatility of the firm R & D investment: Revisited from the perspective of technological capability — 동일 저자팀 (Hayoung Park, Taewon Kang, 이정동) 의 비대칭 매출 충격에 대한 TC 조절 mechanism 의 환경적 stress test 가 본 paper. R&D 지속성 가설의 이론적 토대는 Dierickx and Cool (1989) 의 time compression diseconomy, Bernstein and Nadiri (1989), Himmelberg and Petersen (1994), Hall (2002) 의 조정비용 라인, Brown and Petersen (2011) 의 cash holdings 기반 R&D 스무딩, Bloom (2007) 의 caution effect under uncertainty. R&D 변동성 가설은 Mudambi and Swift (2011, 2014), Swift (2013) 의 proactive R&D management 라인. 위기 환경 prior research 는 Eberhart et al. (2004), Amore (2015), Paunov (2012), Hud and Hussinger (2015), OECD (2012). 추정 방법론은 Hausman and Taylor (1981). 기술경영경제정책전공 의 sibling 으로 R&D activities for becoming a high-growth firm through large jumps: evidence from Korean manufacturing (large jump 의 진입 vs 유지 단계 비대칭) 와 Effects of knowledge accumulation strategies through experience and experimentation on firm growth (지식 experience-experimentation 단계 의존) 가 동일 anchor 의 cross-section 분화로 Chulwoo Baek 가 듀크성 여대 이동 후 협업 cohort 와 함께 정합한다.

See also

- 이정동

- Taewon Kang

- Hayoung Park

- Hausman-Taylor 추정량

- R&D 지속성

- R&D 변동성

- R&D 스무딩

- R&D 동학

- 경제 위기

- 글로벌 금융위기

- 석유화학 산업

- The persistency and volatility of the firm R & D investment: Revisited from the perspective of technological capability

- R&D activities for becoming a high-growth firm through large jumps: evidence from Korean manufacturing

- Effects of knowledge accumulation strategies through experience and experimentation on firm growth

인접 그래프

- 인물 4

- 개관 1

- 방법론 3

- 주제 9

- 수록처 1

- 분류 2

- 논문 3