Technological Diversification through Corporate Venture Capital Investments: Creating Various Options to Strengthen Dynamic Capabilities

Simon U. Lee, 강진아 (2015) · Industry and Innovation 22(5):349-374 · DOI ↗

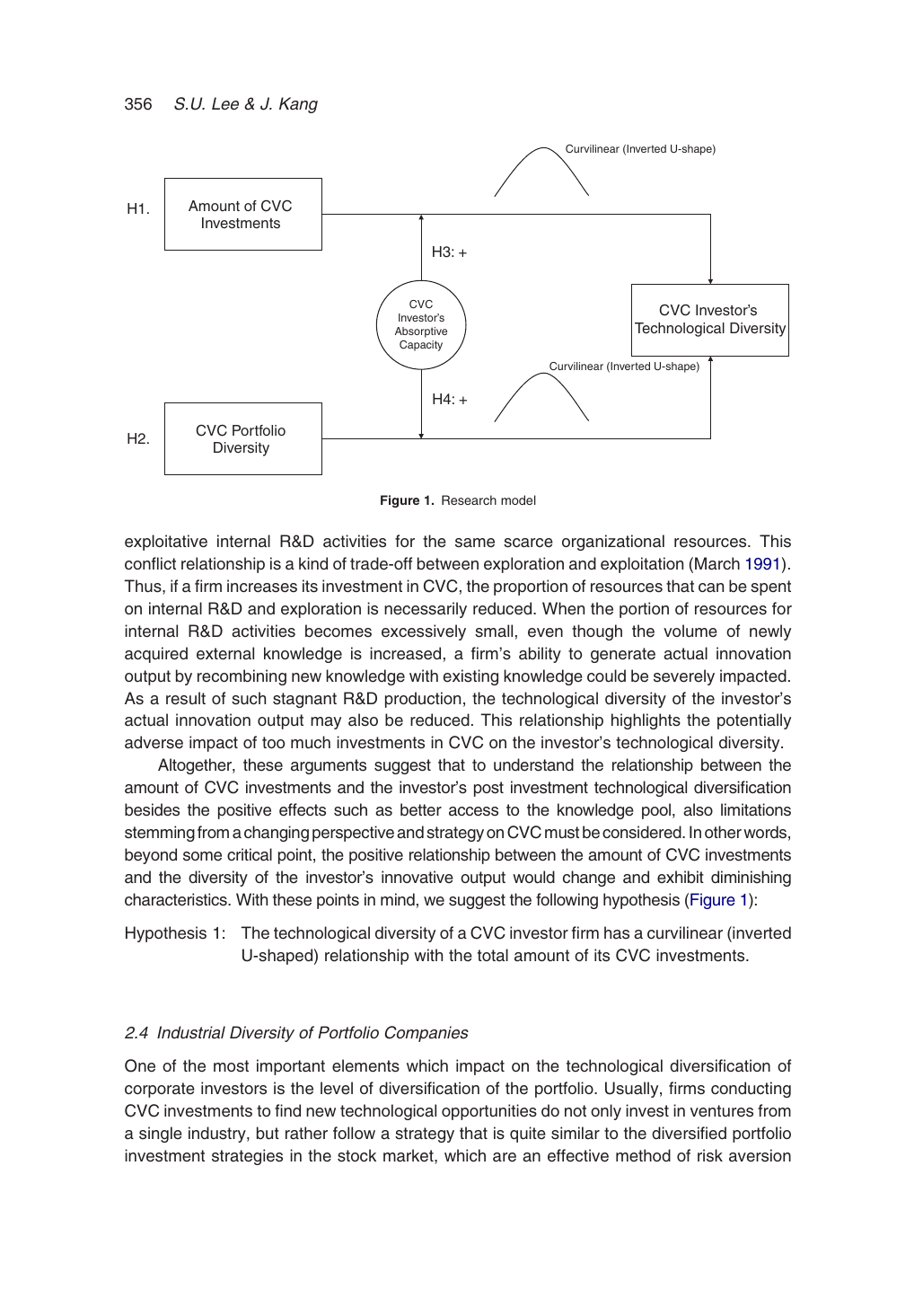

CVC (CVC) 투자는 신생 기업의 다양한 기술 옵션에 소액·유연 지분 투자를 분산해 모기업의 기술 다각화 (technological diversification) 와 동태적 역량 를 강화하는 학습 전략이다. 5개 high-tech 산업 1,313 firm-year 패널 (1990-2010) 을 음이항 회귀 으로 분석해, CVC 총 투자액과 portfolio 산업 다양성이 모두 모기업의 기술 다각화 (3-digit IPC class 수) 와 역-U자 관계를 보임을 확인. 흡수능력 가 portfolio 다양성 효과의 양(+) 기울기를 강화한다.

- RQ: CVC 총 투자 규모와 portfolio 산업 다양성은 corporate investor 의 기술 다각화에 어떤 비선형 효과를 가지며, 흡수역량은 어떻게 조절하는가?

- 방법론: 음이항 회귀, 패널 분석 (random effects), 허핀달 지수

- 데이터: 5개 high-tech 산업 (communication, computer equipment, semiconductor, biotech, medical/pharma) 97개 CVC investor, 1,313 firm-year, 1990-2010 (SDC Platinum, ThomsonOne, USPTO, Datastream)

- 주요 발견: CVC 총 투자액 → 기술 다각화: 선형항 +, 제곱항 - (p<0.001, H1 지지). Portfolio 산업 다양성 → 기술 다각화: 선형항 +, 제곱항 - (p<0.01, H2 지지). 흡수역량 × portfolio 다양성: 선형 -, 제곱 + (p<0.01, H4 지지). 흡수역량 × CVC 총액: H3 부분 지지.

- 시사점: CVC 는 실물옵션 이론 관점의 옵션 창출 메커니즘이지만 일정 임계점 초과 시 통합·관리 비용·인지 과부하 (information overload) 로 다각화 효과 감소. 흡수역량 축적이 ambidextrous 학습의 전제 조건.

요약

기존 CVC 문헌 (Dushnitsky 와 Lenox 2005, Wadhwa 와 Kotha 2006) 은 CVC 가 모기업 혁신 양적 성과 에 미치는 영향을 다뤘으나, 기술 다각화 옵션 창출 메커니즘의 실증은 미흡했다 (Yang, Narayanan, De Carolis 2014). 이 논문은 동태적 역량 (Teece, Pisano, Shuen 1997) 와 양손잡이 전략 (March 1991) 프레임에 실물옵션 이론 이론 (Kogut 1991, Maula 2001) 을 결합해, CVC 가 작은 규모·유연 계약 의 특성으로 미래 기술 패러다임 전환에 대비한 옵션 portfolio 를 구성하는 수단임을 이론화한다.

CVC 가 M&A·alliance 와 차별화되는 세 가지 특징을 정리한다: (1) 전략적 목표가 early-stage emerging technology 식별·평가 에 있고 (Ernst & Young 2008-09 survey 65%), (2) 소액 지분의 유연 계약으로 high-uncertainty 영역에 적합하며, (3) 투자 대상 venture 가 유연한 문화 (Kortum 과 Lerner 2000) 와 emerging market 진입 (Shane 2001) 으로 fresh knowledge 창출 확률이 높다. 5개 high-tech 산업 1,313 firm-year 패널 (1990-2010, USPTO + ThomsonOne + Datastream) 을 음이항 회귀 (random effects) 으로 분석. 종속변수는 3-digit IPC class 의 3년 누적 신규 patent 수 (Wadhwa 와 Kotha 2006), 핵심 독립변수는 CVC 총 투자액 (자연로그) 와 portfolio 산업 다양성 (4-digit VEIC 의 1/HHI), 조절변수는 흡수역량 (R&D 지출 / 자산).

결과는 두 비선형 관계와 한 조절 효과로 정리된다. (1) CVC 총액 → 기술 다각화 = 역-U (β1=+, β2=-, p<0.001) — 초기에는 due diligence 와 board 권한 확대로 지식 풀 접근성이 증가하지만, 임계점 후엔 투자 패턴이 concentration 으로 전환되고 내부 R&D 자원과 trade-off 발생. (2) Portfolio 산업 다양성 → 기술 다각화 = 역-U (β1=+, β2=-, p<0.01) — 다양한 산업 venture 가 distant search (Rosenkopf 와 Nerkar 2001) 를 가능하게 하지만, over-diversification 은 조정 비용 (Argyres 1996) 과 인지 과부하 (Wadhwa 와 Kotha 2006) 를 발생. (3) 흡수역량은 portfolio 다양성의 제곱항 양(+) 조절 — 흡수역량이 클수록 over-diversification penalty 의 곡률이 완만해져 옵션-옵션 활용의 ambidextrous 학습 가능. Reverse causality 검정 (Table 3) 으로 인과 방향 확인. 강진아 의 SNU 이론기 (2-3기) 에서 외부 학습 라인을 alliance → CVC 로 확장한 핵심 작업이며, The double-edged effects of the corporate venture capital unit's structural autonomy on corporate investors' explorative and exploitative innovation (CVC 조직 자율성) 의 직접 선행자.

핵심 결과

| 가설 | 변수 | 부호 | 유의수준 | 해석 |

|---|---|---|---|---|

| H1 | CVC 총액 (linear) | + | p<0.001 | 초기 양(+) |

| H1 | CVC 총액 (squared) | - | p<0.001 | 임계점 후 감소 → 역-U |

| H2 | 산업 다양성 (linear) | + | p<0.01 | 초기 양(+) |

| H2 | 산업 다양성 (squared) | - | p<0.01 | 임계점 후 감소 → 역-U |

| H3 | 흡수역량 × CVC 총액 (sq) | + | p<0.05 | 부분 지지 |

| H4 | 흡수역량 × 산업 다양성 (sq) | + | p<0.01 | 지지 |

표본: 97 CVC investor, 1,313 firm-year (1990-2010), 5개 high-tech 산업. 종속변수 평균 104.6 patent class, SD 135.1.

방법론 노트

종속변수가 over-dispersed count 라 random-effects 음이항 회귀 (Hausman test 기반). 핵심 측정:

여기서 는 firm 의 portfolio venture 중 산업 의 비중 (4-digit VEIC), 역수를 취해 값이 클수록 다양성이 큰 방향으로 정렬 (Leten et al. 2007).

(Cohen 과 Levinthal 1990, Lin et al. 2012). Patent 측정은 patent 신청에서 등록까지 시차 (Hausman, Hall, Griliches 1984) 를 반영해 3년 누적 lag 사용. Reverse causality 검정 (Table 3) 으로 “기술 다각화 → CVC” 역방향 효과 부재 확인.

연구 계보

David J. Teece, Pisano, Shuen (1997) dynamic capabilities, March (1991) exploration-exploitation, Absorptive Capacity: A New Perspective on Learning and Innovation 의 absorptive capacity, Kogut (1991) · Mitchell 과 Singh (1992) · Vanhaverbeke et al. (2002) 의 real options as small initial investments, Gompers 와 Lerner (2000), Dushnitsky 와 Lenox (2005), Wadhwa 와 Kotha (2006), Maula, Keil, Zahra (2003, 2013), Benson 과 Ziedonis (2009), Van de Vrande 와 Vanhaverbeke (2013) 의 CVC 실증 문헌, Mowery, Oxley, Silverman (1998), Giuri, Hagedoorn, Mariani (2004), Leten, Belderbos, Van Looy (2007) 의 alliance ↔ technological diversification 연구를 종합한다. 강진아 author page 의 실타래 3 (탐험 vs 활용의 조직 설계) 의 첫 작업으로, alliance portfolio 다양성 효과를 다뤄 온 라인 (Alliance Addiction: Do Alliances Create Real Benefits?, External Technology Acquisition: A Double-Edged Sword) 의 비선형·“양날의 검” 패턴을 CVC sector 로 옮긴다. 후속 The double-edged effects of the corporate venture capital unit's structural autonomy on corporate investors' explorative and exploitative innovation 가 CVC 조직 자율성 설계 측면을 다뤄 완결한다.

See also

- 강진아

- Simon U. Lee

- Industry and Innovation

- CVC

- 기술 다각화

- 실물옵션 이론

- 동태적 역량

- 양손잡이 전략

- 흡수능력

- 음이항 회귀

- The double-edged effects of the corporate venture capital unit's structural autonomy on corporate investors' explorative and exploitative innovation

인접 그래프

- 인물 3

- 방법론 4

- 개념 5

- 수록처 1

- 분류 1

- 논문 7

이 문서를 가리키는 페이지

논문 (4)

- Complementary or conflictory? The effects of the composition of the syndicate on venture capital-backed IPOs in the US stock market

- The double-edged effects of the corporate venture capital unit's structural autonomy on corporate investors' explorative and exploitative innovation

- The Effects of Ambidextrous Alliances on Product Innovation

- Unravelling the Link between Technological M&A and Innovation Performance Using the Concept of Relative Absorptive Capacity