The double-edged effects of the corporate venture capital unit's structural autonomy on corporate investors' explorative and exploitative innovation

Simon U. Lee, Gunno Park, 강진아 (2018) · Journal of Business Research 88:141-149 · DOI ↗

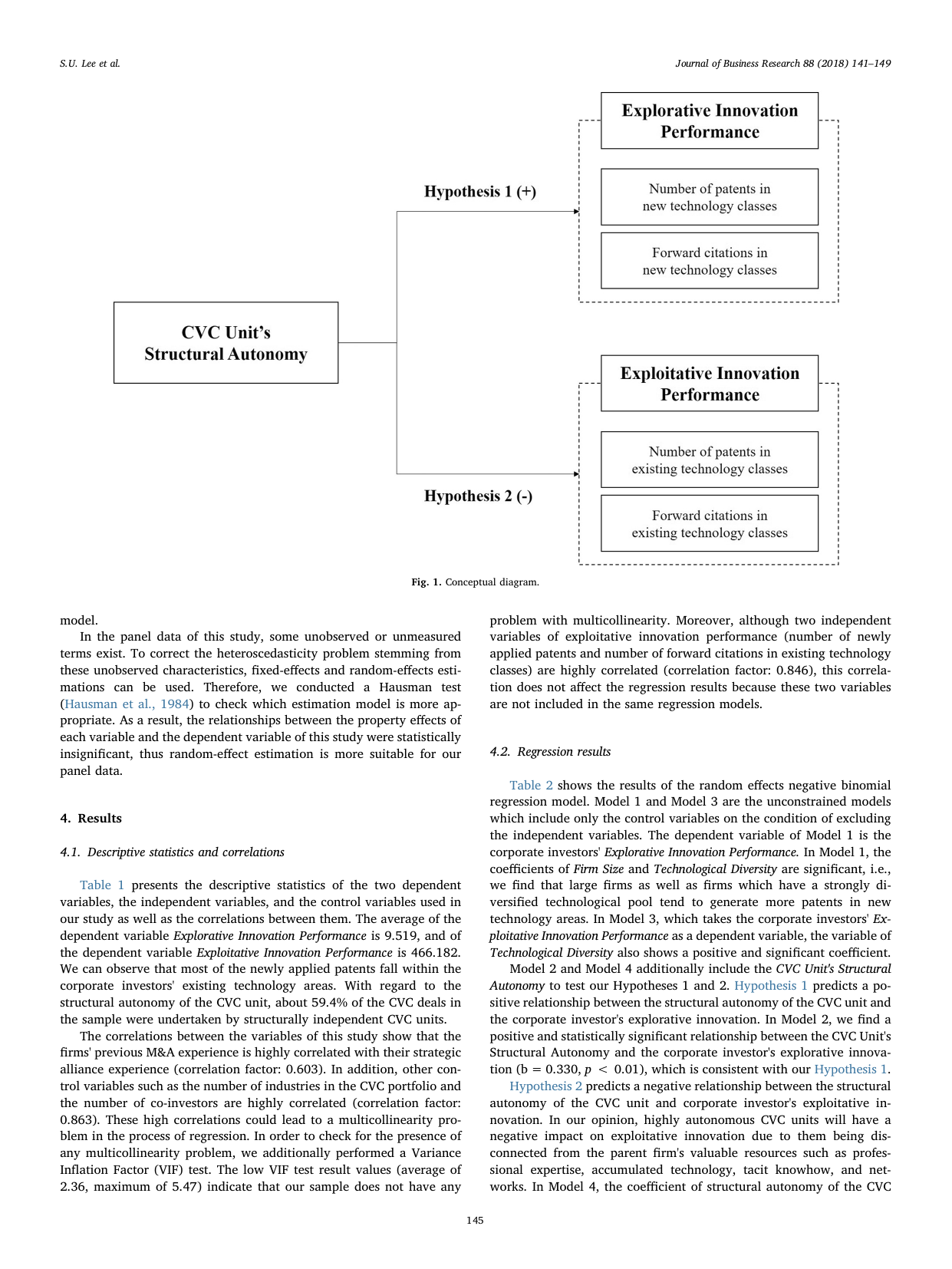

모기업의 CVC (CVC) 전담 조직이 갖는 구조적 자율성 (structural autonomy) — 모기업 직접 투자 vs wholly-owned 독립 subsidiary — 이 모기업의 탐험적 혁신과 활용적 혁신에 어떻게 반대 방향 으로 영향을 주는지 묻는다. 1990–2010 미국 하이테크 7개 산업 77개 corporate investor 의 unbalanced 패널 (318 firm-year, ThomsonOne VentureXpert + USPTO + Compustat + Datastream), random-effect 음이항 회귀 (Hausman test) 결과: 자율성 ↑ → 탐험적 특허 ↑ (, H1), 활용적 특허 ↓ (, H2). 동일 조직 설계가 양손잡이 전략 의 두 축에 정반대로 작동.

- RQ: CVC 전담 조직의 구조적 자율성이 모기업의 탐험적 혁신 과 활용적 혁신 에 대칭적으로 작용하는가, 아니면 양날의 검 (반대 방향) 으로 작용하는가?

- 방법론: 패널 분석, 음이항 회귀, 특허 분석

- 데이터: 미국 하이테크 7개 산업 (computer/IT, electrical/semiconductors, telecom, machinery, chemical/energy, biotech/pharma, other tech services), 77개 corporate investor 의 unbalanced 패널, 1990–2010, 318 firm-year; ThomsonOne PE/VC (VentureXpert) + USPTO IPC 3-digit + Compustat + Datastream

- 주요 발견: H1 자율성 → 탐험적 특허 ; H2 자율성 → 활용적 특허 ; forward citation 종속변수 robustness 도 동일 (, p<.05 / p<.01); 표본 평균 탐험 9.52건 / 활용 466.18건 / 자율성 dummy 59.4% / firm size (log) 9.11 / R&D (log) 6.45

- 시사점: CVC 조직 설계는 전략적 목적 에 정렬돼야. 탐험적 학습 (Google Ventures: Android·smartphone·renewable energy·bio·organic agriculture 분산 portfolio) 이 목표면 자율성 ↑, 활용적 학습 (Cisco Investments: big data·cloud·IoT 등 기존 네트워크 사업 보강) 이 목표면 자율성 ↓. “자율성은 무조건 좋다” 라는 처방은 오답

요약

기존 CVC 연구 (Dushnitsky 와 Lenox 2005, 2006; Wadhwa 와 Kotha 2006; Basu, Phelps, Kotha 2011; Burgelman 1983, 1985; Kanter 1985) 는 CVC 를 탐험적 학습 도구 (window on new technology) 로만 다뤘다. 그러나 NIST · Ernst & Young Global CVC Survey 와 Hill·Birkinshaw (2014), Battistini, Hacklin, Baschera (2013), Markham et al. (2005) 의 in-depth interview 결과 실무에서는 활용적 학습 (supporting existing business) 도 동등한 비중으로 추구된다. Samsung 의 voice recognition (스마트폰 사업 보강) vs food·bio-health care (분산) 양쪽 portfolio, Intel 의 related vs unrelated 분산 investment 가 사례. 이 paper 는 March (1991) 의 탐색-활용 / 양손잡이 전략 와 Burgelman (1984, 1985) 의 internal corporate venturing 을 결합해, 동일 조직 변수 — structural autonomy — 가 두 축에 반대 방향으로 작동한다는 비대칭 가설을 도출한다.

이론: 자율성 높은 CVC unit (wholly-owned subsidiary) 은 모기업 strategic attention 으로부터 독립적이라 (i) 별도 fund pool, (ii) 단기 매출과 무관한 disruptive target 투자 가능, (iii) 모기업 사업 잠재 경쟁자도 투자 가능 → 탐험적 학습 (Siegel, Siegel, MacMillan 1988; Birkinshaw 와 Hill 2005; Chesbrough 2002; Yang, Chen, Zhang 2016). 반면 활용적 학습은 모기업의 축적된 기술·전문가·network resources 와의 근접성 이 필수 (Hoang 과 Rothaermel 2010; March 1991; Cohen 과 Levinthal 1990; Carnabuci 와 Operti 2013) → 자율성 ↑ 이면 이 resource link 가 끊김. Gupta, Smith, Shalley (2006): “exploration 과 exploitation 의 learning·resources·routines 는 다르다.” H1: 자율성 → 탐험 (+); H2: 자율성 → 활용 (−).

방법: VentureXpert dichotomous 측정 (Yang, Chen, Zhang 2016; Kang 과 Park 2015 ws) — 모기업 내부 program (0) vs wholly-owned independent subsidiary (1), firm-year 평균으로 0~1 연속화. 탐험 vs 활용 분리 측정: 새 patent 의 IPC 3-digit primary class 가 (a) 기업의 기존 class pool 밖 (Wadhwa 와 Kotha 2006) 이면 탐험, (b) 안 이면 활용. 3년 cumulative lag (t to t+2) 으로 R&D pipeline 시간차 반영. Random-effect NBR (over-dispersion: 종속변수 SD > mean, Hausman test 으로 random > fixed). Control: firm size (log sales t−1), R&D (log expenditure t−1), M&A·alliance experiences, technology diversity, CVC investment amount, portfolio industry 수, co-investor 수 (quality proxy), 산업 dummy. VIF 평균 2.36, max 5.47. Robustness: forward citation 종속변수, 동일 부호 유지. 강진아 author page 의 2기 (2013–2018) 외부 지식 탐색의 구조적 역학 시기, “양날의 검” 시그니처 패러다임의 CVC × 조직 설계 영역 완성 작업. 같은 라인 출발점 Technological Diversification through Corporate Venture Capital Investments: Creating Various Options to Strengthen Dynamic Capabilities (I&I, real options 관점) 의 후속.

핵심 결과

| 가설 | 종속변수 | β | 유의수준 | 지지 |

|---|---|---|---|---|

| H1 | Explorative patents (count) | +0.330 | p<.01 | 지지 |

| H2 | Exploitative patents (count) | −0.257 | p<.05 | 지지 |

| H1 robust | Explorative forward citations | +0.320 | p<.05 | 지지 |

| H2 robust | Exploitative forward citations | −0.418 | p<.01 | 지지 |

표본 평균: explorative patents (3yr cum) 9.52, exploitative patents 466.18, autonomy dummy 0.594, firm size (log sales) 9.11, R&D (log) 6.45, M&A experiences 4.69, alliance experiences 6.30, technology diversity 0.81, CVC investment amount 3.17, portfolio industries 4.34. N = 318 firm-year, 77 firms, VIF max 5.47.

방법론 노트

종속변수 (3년 누적 patent count) 의 over-dispersion (탐험 SD 9.54 ≈ mean 9.52, 활용 SD 669 > mean 466) 때문에 Poisson 부적합, NBR 채택. Hausman test (Hausman, Hall, Griliches 1984) 로 random-effect 가 fixed 보다 fit 우월. 핵심 회귀식:

여기서 는 탐험적 또는 활용적 patent count (또는 forward citation 수, robustness), 는 firm 의 년 CVC deals 중 wholly-owned subsidiary 비율 [0,1], 는 control. 식별: 동일 firm 의 자율성 변화 (random effect 통제 후) 가 두 종속변수에 정반대 부호로 나오면 비대칭 입증. 3년 lag 는 patent application 의 R&D timeline (Hausman, Hall, Griliches 1984) 반영. 한계: dichotomous 측정이 unit autonomy 의 재무 / 인적 / 의사결정 권한 차원 을 분리 못 함, target firm patent flow 미관측.

연구 계보

직접 선행은 Dushnitsky 와 Lenox (2005, 2006), Wadhwa 와 Kotha (2006), Basu, Phelps, Kotha (2011), Schildt, Maula, Keil (2005) 의 CVC ↔ 탐험적 혁신, Hill 과 Birkinshaw (2008, 2014) 의 CVC 조직 설계 분류, Yang, Chen, Zhang (2016) 의 dichotomous 자율성 측정, Birkinshaw 와 Hill (2005), Siegel, Siegel, MacMillan (1988), Gompers 와 Lerner (2001) 의 CVC governance, Chesbrough (2002) 의 CVC 4 유형. 이론 anchor 는 March (1991) 의 탐색-활용 / 양손잡이 전략, Burgelman (1983, 1985) 의 internal corporate venturing, Teece, Pisano, Shuen (1997) 의 dynamic capabilities, Cohen 과 Levinthal (1990) 의 흡수능력, Gupta, Smith, Shalley (2006), Lavie, Stettner, Tushman (2010), Raisch 와 Birkinshaw (2008) 의 ambidexterity 전략. 강진아 author page 의 2기 (2013–2018) 외부 지식 탐색의 구조적 역학 시기, 실타래 3: 탐험 vs. 활용의 조직 설계 라인 — Technological Diversification through Corporate Venture Capital Investments: Creating Various Options to Strengthen Dynamic Capabilities (I&I, real options) → 본 작업 조직 설계 완성 → Influence of alliance portfolio diversity on innovation performance: the role of internal capabilities of value creation (포트폴리오 다양성 통합) 으로 이어지는 라인. 같은 시기 sibling: The Effects of Ambidextrous Alliances on Product Innovation (양면적 제휴), Complementary or conflictory? The effects of the composition of the syndicate on venture capital-backed IPOs in the US stock market (VC syndicate).

See also

- 강진아

- Simon U. Lee

- Gunno Park

- Journal of Business Research

- CVC

- 양손잡이 전략

- 탐색-활용

- 외부 지식 탐색

- structural-autonomy

- double-edged-sword

- 패널 분석

- 음이항 회귀

- Technological Diversification through Corporate Venture Capital Investments: Creating Various Options to Strengthen Dynamic Capabilities

- Influence of alliance portfolio diversity on innovation performance: the role of internal capabilities of value creation

인접 그래프

- 인물 3

- 방법론 3

- 개념 5

- 수록처 1

- 분류 1

- 논문 5

이 문서를 가리키는 페이지

논문 (5)

- Alliance Addiction: Do Alliances Create Real Benefits?

- Complementary or conflictory? The effects of the composition of the syndicate on venture capital-backed IPOs in the US stock market

- Influence of alliance portfolio diversity on innovation performance: the role of internal capabilities of value creation

- Technological Diversification through Corporate Venture Capital Investments: Creating Various Options to Strengthen Dynamic Capabilities

- The Effects of Ambidextrous Alliances on Product Innovation