The Effect of Asset Composition Strategy on Venture Capital Firm Efficiency: An Application of Data Envelopment Analysis

E.J. Jeon, 이정동, Y.-H. Kim (2009) · Productivity, Efficiency, and Economic Growth in the Asia-Pacific Region Ch. 6, pp. 123–141

한국 Venture Capital 산업의 조성-실패 narrative 를 firm-level efficiency 분석으로 정량화. 100–140 VC firm × 2000–2005 (810 obs, 359 효과 obs) 의 financial statement 위에서 Output-oriented VRS DEA 로 efficiency 추정 후 Fixed effects Tobit 모형 회귀. 핵심 발견: (H1) 초기단계 (early-stage) 투자 → 낮은 efficiency — VC investment asset ratio −0.022*** (efficient firm 일수록 후기단계 투자); (H2) 단기 투자 → 높은 efficiency — current asset ratio +0.039** (efficient firm 일수록 단기 자산). 두 hypotheses 모두 accepted — 즉 한국 VC firm 의 efficient strategy 가 사회적 기대 (초기 + 장기 = high tech 육성) 와 정반대 방향. 정책 함의: (i) 법적 incentive 로 VC firm 의 screening + monitoring 기능 활성화, (ii) 공적 자본 (pension fund 등) 의 risky venture 자본 공급, (iii) US 의 pension fund liberalization (1979 prudent man rule) 같은 institutional reform.

- RQ: 한국 Venture Capital firm 의 efficiency 를 결정하는 asset composition 전략은 무엇이며, 그 efficient 전략이 한국 venture policy 의 사회적 기대 (초기단계 + 장기투자 high tech 육성) 와 부합하는가?

- 방법론: Output-oriented VRS DEA (Banker-Charnes-Cooper 1984 의 variable returns to scale) — 비용 1 종 input + 매출 1 종 output, super-efficiency 로 outlier 제거 후 정상 분포; Fixed effects Tobit 모형 — Hausman test 결과 fixed effects 채택, dependent variable censored at upper limit of 1

- 데이터: 한국 100–140 VC firm 의 2000–2005 panel (FSC 감독원 statement), unbalanced 810 obs → super-efficiency 외부값 제거 → all sample 361 / >3 년 sample 259. Asset 구조: current asset · VC investment asset (early-stage) · management support asset · operation asset (late-stage) · current/non-current ratio · cash outflow ratio

- 주요 발견: All sample Tobit Model II (Table 6.6) — Log current asset ratio +0.039** (단기 자산 증가 → efficiency 상승), Log VC investment asset ratio −0.022*** (early-stage 투자 → efficiency 하락), Log operation asset ratio +0.004** (late-stage 투자 → efficiency 상승); Year 2002 −0.574*** (외환위기 이후 모든 firm efficiency 하락); >3 년 sample (Table 6.8) 결과 동일 방향; current/non-current ratio 도 단기 효과 robust check 양 (+0.032**); cash outflow ratio (=early/late 비율의 proxy) 음 (−0.020***)

- 시사점: 한국 VC firm 의 efficient profit-maximizing 전략 ≠ 사회적 기대 — VC firm 이 banking 수준의 위험회피 로 진화한 institutional failure 의 정량 evidence. 정책 함의: (i) 법적 screening · monitoring 기능 부여 (현재 board membership 제약 완화), (ii) public pension fund 의 risky venture 자본 공급, (iii) 1979 US prudent man rule 같은 institutional reform 으로 long-term risky 자본 pool 형성

요약

한국 Venture Capital 시장은 1981 년 KTB Network 설립 이후 정부 주도로 형성됐다. Kim Dae-jung 정부 (1998–2003) 의 “Special Act to Foster High Tech Firms” (1997) 와 KOSDAQ (1996) 의 개장으로 VC 시장이 압축 성장. 그러나 외환위기 + dotcom bust 후 정부가 인지한 문제 — 단기 rent-seeking + moral hazard + 정치-기업 결탁 (Ji 2006) — 외에 더 근본적 문제 는 VC firm 자체의 risk-controller · high-tech firm manager 역할 부재. 한국 VC firm 은 low-risk low-return 의 banking-like 행동 패턴 (Park 1997, Kwak 2001, Chung-Ryou 2004) 을 보이며, 본 paper 의 motivation 은 왜 그러한가 의 firm-level 정량 진단.

방법론은 두 단계. Step 1: DEA efficiency 추정. Output-oriented VRS DEA (Banker-Charnes-Cooper 1984) — 한국 VC firm 의 output control 우위 (입력 = 정부·투자자 fixed allocation, 출력 = 운영 수익) 가정에 맞춤. Input = 영업 비용 + 투자·금융 비용, Output = VC fund · high tech firm 투자 수익 + 기타. Super-efficiency 로 outlier 10–15% 제거 → 정상 분포 efficiency score. Step 2: Tobit 회귀. Asset composition ratio 를 설명변수, efficiency score 를 dependent (censored at 1) 로 Fixed effects Tobit 모형 추정. Hausman test 가 fixed effects 지지.

핵심 가설 (Fig. 6.3):

- H1 (Early vs Late stage): 초기단계 투자 (VC investment asset) 가 후기단계 투자 (operation asset) 보다 낮은 efficiency 를 보일 것. Stinchcombe (1965) 의 liability of newness, Phillips-Kirchhoff (1988) 의 4 년 생존확률, Gupta-Sapienza (1992) 의 early-stage 위험 4 유형 (demand · technological · resource · management uncertainty) 의 lineage. 한국 법은 VC firm 의 board member · managerial assistance 제약 → early-stage risk 통제 어려움.

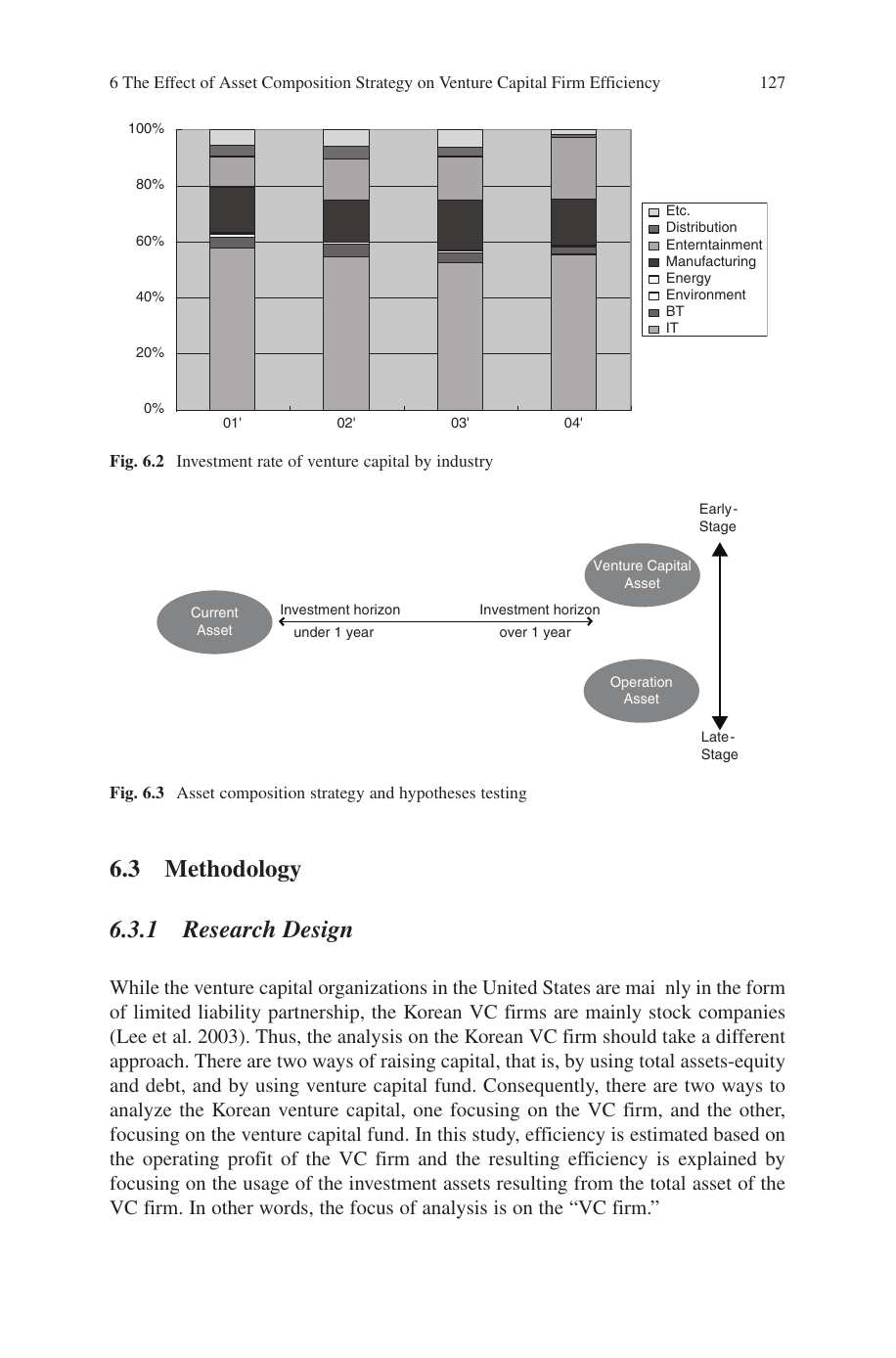

- H2 (Short vs Long term): 단기 투자 (current asset) 가 장기 투자 (non-current asset) 보다 높은 efficiency. Petty et al (1994) 의 investment horizon 증가 → return 감소 가설. 한국 VC firm 의 IT · entertainment · manufacturing focus 와 BT · ET 회피 패턴 (Fig. 6.2).

추정 결과 (Table 6.6 의 all sample Model II): (H1 confirmed) Log VC investment asset ratio −0.022*** — early-stage 투자가 efficiency 를 강하게 낮춤; Log operation asset ratio +0.004** — late-stage 투자가 efficiency 를 양으로 contribute. (H2 confirmed) Log current asset ratio +0.039** — 단기 자산 증가가 efficiency 를 7 배 더 끌어올림 (current/non-current ratio 의 0.032 효과 대비). Log cash outflow from operation to investment ratio −0.020*** (Model IV) — early/late stage 의 역방향 proxy 로 robustness 확인. Year dummy 모두 음으로 강하게 유의 (Year 2002 가 −0.574*** 로 가장 큰 음 — 외환위기 직후의 system-wide efficiency 위축). >3 년 sample (Table 6.8) 의 추정 결과 동일 방향 — young VC firm 의 투자 horizon 부족 가설 기각, systemic pattern 확인.

저자의 결론 narrative 는 strong: 한국 VC firm 의 efficient profit-maximizing 전략 ≠ 사회적 기대. VC firm 이 “low marginal cost of capital + 잠재 성공 firm screening + monitoring 으로 value-add” 라는 책 같은 정의 와 정반대 — 한국 VC firm 은 late-stage + 단기 투자 의 banking-like profit-maximizing 으로 evolved. Venture policy 실패 의 institutional root: 자본 시장 형성기에 loan 시장의 short-term · late-stage focus 가 그대로 VC 시장으로 transfer 됐고, 정부 정책은 이를 corrected 못함. 정책 제안: (i) 법적 screening · monitoring 기능 부여 (현 제약 완화 + VC firm 의 board membership 허용 + 산업 정보 접근), (ii) public pension fund 의 risky venture 자본 공급 — US 의 1979 prudent man rule 의 한국 version (1990–2002 미국 신규 자본의 44% 가 pension fund), (iii) early-stage · 장기 specialized VC 의 institutional support. 한계는 (i) DEA 의 input/output 선택 (operating 접근 vs intermediation 접근 vs production 접근) sensitivity, (ii) cross-section panel 의 short horizon (6 년), (iii) social return 측정 부재 — efficient VC 가 사회적 손실 인지 사회적 가치 인지의 normative judgment 가 암시 만 됨.

핵심 결과

Asset 분류 (Table 6.2 단순화)

| 분류 | 구성요소 | 본 paper 가정 |

|---|---|---|

| Current assets | 현금 · 단기 채권 · 단기 투자 | 단기 + 일반 |

| VC investment assets | 주식 · 전환사채 · project 투자 · venture fund | 초기단계 high-risk |

| Management support assets | committed stock · startup loan · 해외 투자 · SMB 투자 | 보조 |

| Operation assets | non-committed long-term investment | 후기단계 (7년 이상 firm) |

| Tangible assets | 기계 · 건물 · 토지 | 운영 |

Descriptive statistics (Table 6.4, all sample N=361)

| 변수 | Mean | SD | Min | Max |

|---|---|---|---|---|

| Current asset ratio | 0.24 | 0.19 | 0.003 | 0.93 |

| VC investment asset ratio | 0.45 | 0.25 | ≈0 | 0.99 |

| Management support asset ratio | 0.07 | 0.12 | ≈0 | 0.69 |

| Operation asset ratio | 0.08 | 0.12 | ≈0 | 0.93 |

| Age (months) | 85.4 | 65.0 | 2 | 228 |

→ VC investment ratio (50% 법적 상한) 평균 45%, 큰 분산 (0.25) — risk-averse vs risk-loving VC firm 의 변이.

Fixed effects Tobit 추정 (Table 6.6, all sample Model II)

| 변수 | 계수 | SE |

|---|---|---|

| Log current asset ratio | +0.039** | 0.019 |

| Log VC investment asset ratio | −0.022*** | 0.004 |

| Log management support asset ratio | +0.001 | 0.002 (n.s.) |

| Log operation asset ratio | +0.004** | 0.002 |

Model IV (substitute proxies, Table 6.6)

| 변수 | 계수 | SE |

|---|---|---|

| Log current/non-current asset ratio | +0.032** | 0.015 |

| Log VC investment asset ratio | −0.022*** | 0.004 |

| Log cash outflow ratio (operation/investment, ≈ early/late proxy) | −0.020*** | 0.007 |

→ H1 (early-stage 음) · H2 (단기 양) 모두 두 paired proxy 에서 robust.

Year dummy (외환위기 효과 통제)

| Year (vs 2000) | 계수 |

|---|---|

| 2001 | −0.327*** |

| 2002 | −0.574*** (시스템 충격 최대) |

| 2003 | −0.511*** |

| 2004 | −0.491*** |

| 2005 | −0.276*** |

→ 모든 year 가 base year 2000 대비 음 — 2000 의 dotcom 직전 호황 이후 system-wide efficiency 위축.

>3 년 sample 의 robustness (Table 6.8)

| 변수 | 계수 (Model II) | 일관성 |

|---|---|---|

| Log current asset ratio | +0.033** | 일관 (양) |

| Log VC investment asset ratio | −0.011*** | 일관 (음) |

| Log operation asset ratio | +0.003* | 일관 (양) |

→ Young VC firm 의 horizon 부족 가설 기각, systemic pattern 확인.

방법론 노트

Output-oriented VRS DEA (Banker-Charnes-Cooper 1984) — variable returns to scale 가정:

= 출력의 비례 증가 가능량 (input 고정 시). 한국 VC firm 의 output control 우위 (input = 정부 / 투자자 fixed allocation) 가정에 맞춤. Cooper-Park-Pastor (1999) 의 super-efficiency 로 outlier (efficiency >> 1) 제거 — Banker-Gifford (1988) 의 procedure.

Fixed effects Tobit 모형 (Eq. 6.2):

if , otherwise. censoring at upper limit 1 — efficient firm 의 latent efficiency 가 1 이상이라도 1 로 관측. Maximum likelihood 추정의 likelihood (Eq. 6.3):

Hausman test 의 fixed vs random effects 선택에서 fixed effects 채택 — VC firm individual heterogeneity 가 RHS 변수와 상관.

식별은 (i) 100–140 VC firm × 6 년 panel 의 within-firm 변동, (ii) 외환위기 (2001–2003) 의 time variation 으로 macro 충격 통제, (iii) >3 년 sample 의 subsample 비교에서 horizon robustness 확인에서 온다. 한계는 (i) DEA 의 input/output 선택 sensitivity (operating vs intermediation vs production 접근), (ii) panel 의 short horizon, (iii) social return vs private return 의 normative 분리 어려움.

연구 계보

본 paper 의 VC firm efficiency DEA lineage 는 DEA 의 표준 — Charnes-Cooper-Rhodes (1978), Banker-Charnes-Cooper (1984) — 위에 banking efficiency DEA 응용 lineage (Berger-Hancock-Humphrey 1993, Frexias-Rochet 1997, Sealey-Lindley 1977, Jemric-Vujcic 2002 J. Bus. Econ. Stat., Das-Ghosh 2006) 의 operating approach 채택. Venture capital strategy lineage 는 Gorman-Sahlman (1989 J. Bus. Vent.), Gupta-Sapienza (1992) 의 early-stage risk 분류, Rosenstein-Bruno-Bygrave-Taylor (1990 J. Bus. Vent.) 의 VC value-add, Carter-Auken (1994), Timmons-Sapienza (1992) 의 stage-of-investment shift 가설, Gifford (1997) 의 time-constraint general partner 모형. Resource-based theory 위 lineage 는 Wernerfelt (1984 Strategic Management Journal), Teece-Pisano-Shuen (1997 SMJ), Boeker (1997) 의 firm strategy + resource.

한국 VC 실증 lineage 는 Park (1997), Kwak (2001), Chung-Ryou (2004 한국 외환·금융 연구), Ji (2006) 의 venture moral hazard 분석. 본 paper 의 contribution 은 firm-level efficiency 의 원인 (asset composition) 정량 식별 — 기존 라인은 결과 (low return) 의 documenting 에 머물렀다.

TEMEP 내 sibling: (i) The relevance of DEA benchmarking information and the Least-Distance Measure — 같은 batch 의 DEA 방법론 paper 로 본 paper 의 efficiency 측정 도구의 method anchor. (ii) The Study on the Technology Finance Policy for Technology Development on the Value Chain Based Innovation System — value chain + technology-based SME finance 의 conceptual framework — 본 paper 의 VC firm 의 institutional 실패 진단과 호환. (iii) Strategy of start-ups for IPO timing across high technology industries — IPO timing 분석으로 본 paper 의 VC funding 영향과 paired (BT 에서 VCEquity 가 quick IPO driver). (iv) Total Factor Productivity in Korean Manufacturing Industries · Evaluation of credit guarantee policy using propensity score matching — TEMEP TFP · 정책 평가 라인의 DEA · censored model sibling. 본 paper 는 Productivity, Efficiency, and Economic Growth in the Asia-Pacific Region (J.D. Lee · A. Heshmati 편) Springer 책의 Chapter 6 — 기술경영경제정책전공 의 Asia-Pacific productivity 학술 anchor 책의 일부.

See also

- DEA

- Output-oriented VRS DEA

- Fixed effects Tobit 모형

- Venture Capital

- Asset composition 전략

- 초기 vs 후기 단계 투자

- 단기 vs 장기 투자

- 한국 venture 정책 실패

- The relevance of DEA benchmarking information and the Least-Distance Measure

- The Study on the Technology Finance Policy for Technology Development on the Value Chain Based Innovation System

- E.J. Jeon

- 이정동

인접 그래프

- 인물 3

- 개관 1

- 방법론 3

- 개념 3

- 주제 3

- 수록처 1

- 분류 2

- 논문 11

이 문서를 가리키는 페이지

논문 (8)

- A metafrontier approach for measuring Malmquist productivity index

- Analysis of product efficiency in the Korean automobile market from a consumer's perspective

- Comparative Analysis of Plant Dynamics by Size: Korean Manufacturing

- Corporate Venture Capital and Its Contribution to Intermediate Goods Firms in South Korea

- Economic Impact Assessment of the Government-led Venture Firm Certification Policy

- Evaluation of credit guarantee policy using propensity score matching

- Evaluation Telecenter Performance in Social Sustainability Context: A Cambodia Case Study

- The relevance of DEA benchmarking information and the Least-Distance Measure